1,600 Words / 7 min. Read

The property insurance crisis is becoming a prime mover for climate migration in the US.1,2 As premiums rise and insurers drop policies, it becomes difficult (if not impossible) to buy and sell homes in risk-prone areas, or to rebuild after disaster strikes.3,4 As the New York Times reports:

Without insurance, you can’t get a mortgage; without a mortgage, most Americans can’t buy a home. Communities that are deemed too dangerous to insure face the risk of falling property values, which means less tax revenue for schools, police and other basic services. As insurers pull back, they can destabilize the communities left behind, making their decisions a predictor of the disruption to come.5

It should be clear that climate change is a major factor, and now we have the data to back it up. In 2025, a report from the National Bureau of Economic Research found a strong link between home insurance premiums and climate risk.6 Titled Property Insurance and Disaster Risk, authors Benjamin Keys & Philip Mulder found that premiums have risen over 30% on average since 2020, with at-risk regions seeing much larger increases.7

In this post, we’ve mapped that data so you can see how and where the insurance crisis is affecting America; we’ll also be highlighting some key findings from the report, and looking at which areas of the country have been most affected.

Preface

Before we dive in, it’s important to note that home insurance premiums are not a direct representation of climate risk.7 While they account for disasters that pose a threat to property (like wildfires, floods, hurricanes, and hail), insurers may underweight factors like extreme heat, which pose a severe risk to human health.8,9 Insurance premiums also reflect factors like housing prices and insurance regulations, which aren’t always related to climate risk.10

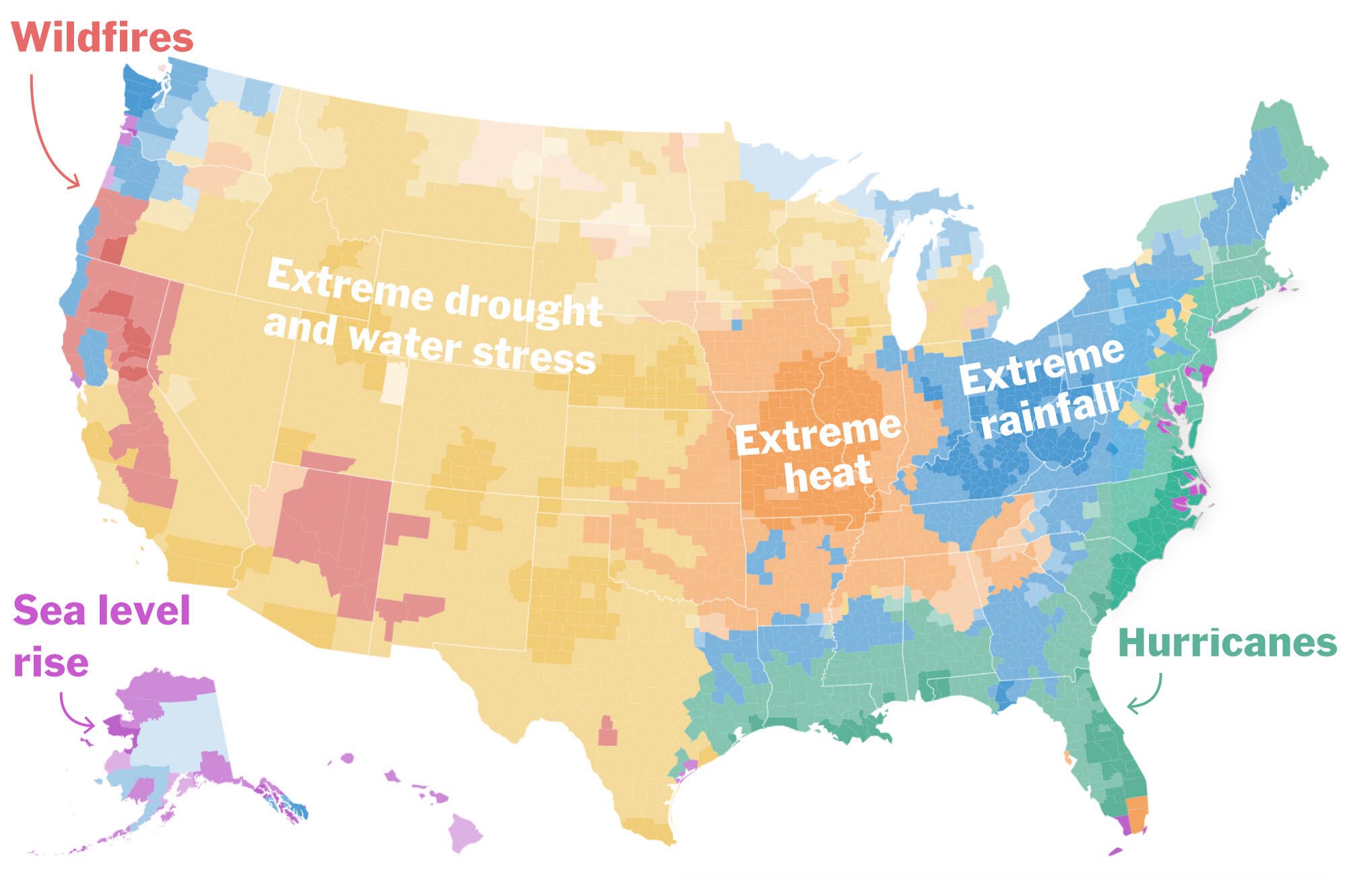

If you’re wondering whether your home is in a high-risk area, we’ve compiled over 80 maps of climate-related threats so you can see your exposure at a glance.

Remember that the primary motive of insurance companies isn’t to protect you from disasters; it’s to maximize profits and shareholder returns.11,12 Despite mounting losses from disasters and extreme weather, property insurers nearly doubled their profits from 2023 to 2024, to the tune of over $171 billion.13

Hurricanes, fires and other disasters caused an estimated $320 billion in losses around the world in 2024, about a third more than the year before. In the US alone, five big hurricanes as well as other severe storms struck.

However, data showed insurers more than offset larger losses by increasing premiums. Helen Andersen, an AM Best research analyst, told the Financial Times that the strong earnings figures were the result of “an aggressive push for significant rate and pricing increases” by insurers.14

When raising premiums isn’t enough, insurers may refuse to renew policies or pull out of states entirely. While moving is a decision that shouldn’t be taken lightly, if you live in one of the regions of America that’s most at risk from climate change, it may be time to start your search for a new home.

Insurance Premiums

This map shows the average yearly cost of insurance premiums by county, from 2020 through 2024:

Our first area of concern is Northern California, specifically the Sierra Nevada region. This is likely due to the severity of wildfire risk in that area,15 which was home to some of the largest and most destructive fires of the past decade (such as the Dixie Fire,16 Camp Fire,17 and Tubbs Fire18). California offers a state-run insurance program (the FAIR plan) to aid homeowners who are unable to find insurance, but plans are typically more expensive and provide less coverage than commercial options.19,20

Moving east, we see a large swath of red across the Great Plains, stretching all the way from northern Texas to North Dakota and Minnesota. According to the report, this is driven mainly by hail and tornado risk across that region.6 As NPR reports:

"Even though tornadoes are a much more significant threat to life, most of the insured damages associated with severe weather come from hail," says Scott St. George, head of weather and climate research at insurance broker WTW. "Tornadoes are awful and they're severe, but the footprint of those storms is usually pretty small."

Hailstorms, on the other hand, cause damage across much larger areas. Hailstones, which can break windows, tear off siding and dent and even puncture roofing material, account for between half and 80% of homeowner insurance claims annually.

"Hail has become an increasing contributor to claims in recent years due to frequency and severity," says Ben Keys, a real estate and finance professor at The Wharton School at the University of Pennsylvania.21

Our third area of concern is the Gulf Coast Region, stretching from eastern Texas through Louisiana, Missouri, and Florida. This should come as no surprise to our readers, as this region consistently ranks highest across multiple climate risk factors. The Gulf coast is facing multiple overlapping risks from climate change, including severe heat, deadly wet bulb temperatures, flooding, hurricanes, and sea level rise.22

Of particular note is the southern tip of Florida, where 2024 premiums in Monroe County hit $9,400/year - the highest in the nation, and nearly 4 times the national average.6 Those figures are due to a combination of high risk and high property values in those areas.23

Our final area of concern is the Eastern Seaboard, which like the Gulf Coast is facing compounding risks from flooding, hurricanes, and sea level rise, which we can see reflected on the map. This is exacerbated by large population centers and high property values in these coastal regions.24,25

Rate Increases

Next, let’s take a look at the rates by which insurance premiums increased from 2014 to 2024:

And from 2020 to 2024:

The biggest increases are found in the western United States; rates in Colorado, Nebraska, South Dakota, and Wyoming have more than doubled over the past 10 years. Arizona, Illinois, Iowa, and Louisiana have been heavily affected as well.

Below is a table showing premiums and rate increases at the state level. (You can click on any column to sort by that value.)

While the report didn’t identify specific reasons for these increases, we can assume that they’re tied to many of the same factors identified in the previous section, with hail and wildfires being the most prevalent in those regions.

Vermont is the only state where premiums decreased, although those percentages come from 2023 figures (no data was available for 2024). Alaska, Maine, New York and New Jersey had the lowest increases across both time periods, while Maine, Nevada, Oregon and Utah had the lowest premiums overall.

Key Takeaways

Average property insurance premiums have risen by more than 30 percent since 2020, and there is wide variation by location. Premiums have risen the most for homeowners in areas with the highest risk of natural disasters such as hurricanes or wildfires.

While premiums have always been higher in riskier locations, the relationship between disaster risk and premiums has grown stronger over time. If present trends in the incidence of natural disasters continue, premiums are likely to continue to rise.26

This report reinforces two key points; first, that we can’t rely on insurance as a hedge against climate change. When disasters mount, insurance companies are likely to raise rates to the point of unaffordability, or withdraw from risk-prone regions entirely.27 Smaller insurers may simply become insolvent or declare bankruptcy.28

Second, that climate-vulnerable regions are becoming financial traps; homeowners in at-risk areas may be forced to choose between paying unaffordable premiums, or paying out of pocket to rebuild their homes.29 Decreasing property values and high premiums discourage new buyers, and homeowners looking to migrate may end up selling their properties at a loss. From the New York Times:

Even after she escaped rising floodwaters by wading away from her home in chest-deep water during Hurricane Rita in 2005, Sandra Rojas, now 69, stayed put. But this year, her annual home insurance premium increased to $8,312, more than doubling over the past four years.

She considered selling, but found herself in a dilemma. As insurance costs have risen, area home values have fallen, dropping by 38 percent since 2020. “They won’t insure you,” Ms. Rojas said. “No one will buy from you. You’re kind of stuck where you are.”29

We’ve stated before that the property insurance crisis is a canary in the coalmine,30 and that it’s quickly becoming a driver of climate migration.31,32 A 2023 report by the First Street Foundation calculated that over 3 million Americans have moved due to flood risk alone, with 7.5 million more to follow over the next 30 years.33,34 As natural disasters and financial crises mount, those trends are likely to accelerate.35

Moving to a new area isn’t a magic bullet; climate resilience is something that’s built across all areas of your life. And since exposure to disasters like fires and floods can vary widely based on topography, most Americans won’t need to move across the country; a less vulnerable location may be found just a few miles away.36,37 But if you live in a high-risk region of America, it may be time to look for higher ground.

In the next post, we’ll take a look at another aspect of the insurance crisis: insurer nonrenewals, or cases where homeowners are unable to extend their policies once they expire.

Footnotes & References

- The Uninsurable Future: The Climate Threat to Property Insurance, and How to Stop It (Dave Jones, The Yale Law Journal)

- Climate change is upending homeowners insurance nationwide (Bill Ainsworth, Susan Milligan, Harvard Business School)

- How is climate change impacting home insurance markets? (Meredith Fowlie, Judson Boomhower, Daniel Richter, Riki Fujii-Rajani, Brookings)

- The Insurance Crisis Continues to Weigh on Homeowners (Steve Koller, Harvard Joint Center for Housing Studies)

- Insurers Are Deserting Homeowners as Climate Shocks Worsen (Christopher Flavelle, Mira Rojanasakul, The New York Times)

- Property Insurance and Disaster Risk: New Evidence from Mortgage Escrow Data (Benjamin Keys, Philip Mulder, NBER)

- Home Insurance Rates in America Are Wildly Distorted. Here’s Why. (Christopher Flavelle, Mira Rojanasakul, The New York Times)

- Weather Related Fatality and Injury Statistics (National Weather Service)

- Extreme heat: What to know about the deadliest climate risk of our time (Tom Crowfoot, PreventionWeb)

- Pricing of Climate Risk Insurance: Regulation and Cross-Subsidies (Sangmin Oh, Ishita Sen, Ana-Maria Tenekedjieva, Journal of Finance)

- A Legal Theory of Shareholder Primacy (Robert Rhee, Harvard Law School)

- The top line is the bottom line in insurance (Nick Palmer, Scott Tanner, Christine Detrick, Ingo Wagner, Bain & Company)

- The Insurance Industry is Quietly Making Record Profits (American Association for Justice)

- US insurers’ profits double as price rises exceed extreme weather claims (Lee Harris, Financial Times)

- Fire Hazard Severity Zones (CAL FIRE)

- Dixie Fire (Wikipedia)

- Camp Fire (Wikipedia)

- Tubbs Fire (Wikipedia)

- California FAIR Plan (California FAIR Plan)

- California FAIR Plan (Wikipedia)

- Insurance costs are soaring around Tornado Alley. Hail is the big problem. (Michael Copley, NPR)

- This Part of the U.S. Will Suffer Most from Climate Change (Daniel Cusick, Scientific American)

- Find out the average price of home insurance in your county (Ron Hurtibise, South Florida Sun Sentinel)

- Northeast megalopolis (Wikipedia)

- Why Coastal Property Values Grow Despite Climate Risks (Martin Smith, Duke University)

- Disaster Risk and Rising Home Insurance Premiums (Laurent Belsie, NBER)

- As climate risks mount, the insurance safety net is collapsing (Lois Parshley, Grist)

- They survived the hurricane. Their insurance company didn’t. (Zoya Teirstein, Grist)

- A Climate ‘Shock’ Is Eroding Some Home Values. New Data Shows How Much. (Claire Brown, Mira Rojanasakul, The New York Times)

- Insurance Companies: Climate’s Canary in the Coal Mine? (Rachel Sbar, Global Center for Climate Justice)

- America’s Great Climate Migration Has Begun. (David Craig, Columbia Magazine)

- Climate-Induced Migration Patterns and Property Insurance (Chia-Chun Chiang, Greg Niehaus, Society of Actuaries Research Institute)

- Climate Abandonment Areas (Jeremy Porter, First Street)

- Integrating climate change induced flood risk into future population projections (Evelyn Shu, Jeremy Porter, Mathew Hauer, Sebastian Sandoval Olascoaga, Jesse Gourevitch, Bradley Wilson, Mariah Pope, David Melecio-Vazquez, Edward Kearns, Nature Communications)

- U.S. Billion-Dollar Weather and Climate Disasters (Climate Central)

- The Data Behind Flood Factor (First Street)

- The Data Behind Fire Factor (First Street)